What is it?

Medicare is the national health insurance program in the U.S. for folks 65 or older. Some other folks younger than 65 can qualify for Medicare too such as those that have certain disabilities and those that have End-Stage Renal Disease (ESRD).

What Does it Cover?

There are several parts to Medicare, each part responsible for providing for a different general area of your health care. Click the links below to read about each part in much more depth.

The block diagram below shows the big picture of Medicare. The only parts in this diagram directly provided by the federal government are Part A and Part B together known as “Original Medicare”. That’s why when you receive your Medicare card from the government, it’s only showing Part A and B on there along with the effective date for each part. The other parts (Part C, Part D, and Medigap) are provided by private insurance companies.

How Much Does it Cost?

Almost everyone that is eligible for Medicare pays $0 as a monthly premium for Part A. In order to qualify for this “premium-free” Part A, either you or your spouse needs to have worked and paid Social Security taxes for 40 total quarters, or 10 years. See Part A for more information about premiums and cost-sharing.

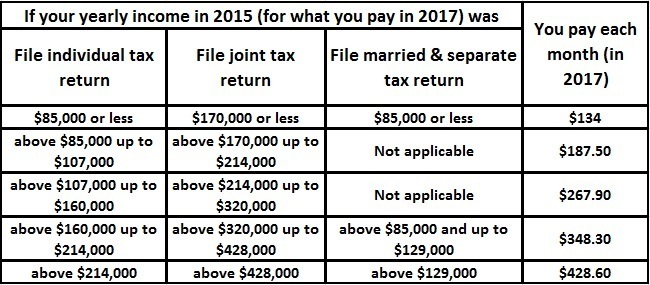

Part B has a monthly premium for everybody, however not everyone pays the same amount. Those who have a Modified Adjusted Gross Income (MAGI) above $85,000 as an individual, or above $170,000 as a married couple filing jointly, will pay more depending on where their exact MAGI falls in the ranges in the chart below. These Medicare beneficiaries have to pay more than everyone else due to what’s called an Income Related Monthly Adjustment Amount (IRMAA).

For those who first become eligible for Medicare in 2018 and are not subject to IRMAA, their Part B premium is $134. For those who started Medicare before 2017 and are not subject to IRMAA, their monthly Part B premium will be less than $134, depending on a few different factors. See Part B for more information about premiums and cost-sharing.

How Do I Pay For It?

If you’re drawing any type of Social Security income, your Medicare Part B premium is taken directly out of your Social Security. If you’re not drawing Social Security when you start Medicare, you will get billed quarterly. So for example, if your Part B premium is $134, your quarterly bill will be $402. Something to note here, however, is that the first Medicare premium bill you receive for Part B can be for more than a 3-month premium payment. However, after this first bill, the bill will be quarterly from then on. If you don’t qualify for premium-free Part A, you will be billed monthly for this also.

Something else to note if you don’t want to have to pay such a large multiple-month bill, or would like to have your Part B premium paid automatically without having to send in a payment, is that you can use Medicare Easy Pay. It’s a free payment option where the Medicare premium is deducted from the bank account of your choice automatically every month. Check out the Medicare Easy Pay page on the Medicare.gov website to learn more or to download the form to apply.

How Do I Sign Up?

If you're drawing any form of Social Security income, whether based on your own record or on the record of someone else (e.g. spouse, ex-spouse, deceased spouse) you will be automatically enrolled in Part A and Part B.

If you are not drawing Social Security, you will need to sign up for Medicare if you want it. You can sign up starting any time after 3 months before your Medicare effective date. There are 3 ways to enroll:

- Online at Medicare.gov -> click the “Apply for Medicare” green button in the upper left part of the page. This is the easiest method. No waiting at the local Social Security office or on the phone. It should take about 10-15 minutes on your computer.

- By calling Social Security at 1-800-772-1213 and enrolling over the phone. This involves a longer time commitment though depending on how busy they are and how long you have to wait on hold to talk to a Social Security agent.

- By going into your local Social Security office. This could involve a time commitment of several hours between the commute and the wait time at the office. If you want to sign up for Medicare this way, I would advise arriving as soon as they open, or making an appointment in advance to save you time.

When Will It Start?

If you are drawing Social Security already and will be automatically enrolled in Medicare, your Medicare effective date will be the first day of the month you turn 65. If you have to sign up for Medicare and do so any time between 3 months prior to this effective date and up to this effective date, Medicare will start on your effective date. If you sign up for Medicare after your first eligible effective date, well now it gets a bit more complicated and it’s better to have a more in-depth discussion about different Medicare Enrollment Periods. The only exception to the “first day of your birth month” rule is if your birthday is on the first of the month; in this case Medicare will start the month before. So, for example, if your birth date is June 1st, 1953, your default Part A and B effective dates will be May 1st, 2018.

For those who qualify for Social Security Disability benefits (SSDI), your Part A and B effective date is the first day of your 25th month of disability benefits. Put a simpler way, after you are eligible for SSDI for 2 years, you’ll automatically be enrolled in Medicare. If you happen to turn 65 before these 24 months elapse, Medicare will start as discussed in the previous paragraph; you don’t have to wait for the full 2 years in that case.

If you will automatically be enrolled in Medicare, you should receive your Medicare card in the mail about 3 and 1/2 months before your effective date. So, for example, if your birthday is November 19th, 1952 and you’re currently drawing Social Security income, you should receive your Medicare card in the mail around the middle of July that same year. If you have to enroll in Medicare on your own, it may take a couple months for you to get your card in the mail, but you’ll often get a letter beforehand confirming that you are signed up and confirming your effective date.

Do I Have To Sign Up?

Not necessarily. If you, or your spouse, are still working and you are covered by that employer’s group health plan, you probably don’t need to sign up for Medicare Part A and B and it might be best for you to wait. As long as that employer has 20 or more employees, Medicare is not required to be the primary insurance. However, make sure your group coverage is considered “creditable coverage” for the prescription coverage. If it’s not and you don’t sign up for a Part D plan when you’re first eligible for Medicare, you’ll likely have to pay a Late Enrollment Penalty (LEP) when you do sign up for Part D later. I’ll go into this in more detail in the section for Part D.

Even if you don’t have to sign up when you’re first eligible, it may be a good idea to check with an insurance professional to look into your healthcare options. Even though you may still be able to stay under your current group’s policy, it might be more cost-efficient to sign up for Medicare Part A and B and enroll in your own supplemental insurances (including Part D). If you’re in this type of situation, contact me to set up a quick consultation and we can discuss your options to decide which is best for you.