Looking for a way to keep your Medigap premiums lower, and still avoid a likely possibility of paying thousands in out-of-pocket expenses in a given year?

Well look no further than Plan N.

But how is Plan N different than Plan F which I’ve heard so much about before? Let’s take a look…

More...

Get a quote on Medigap plans in your area

How it Works

Plan N is a Medigap Plan, also known as a Medicare Supplement. With any Medigap Plan, you have Original Medicare as your primary insurance. So as long as the healthcare provider you go to takes Medicare, they take whatever Medigap insurance you have, it doesn’t matter which insurance company provides it, or what plan you have.

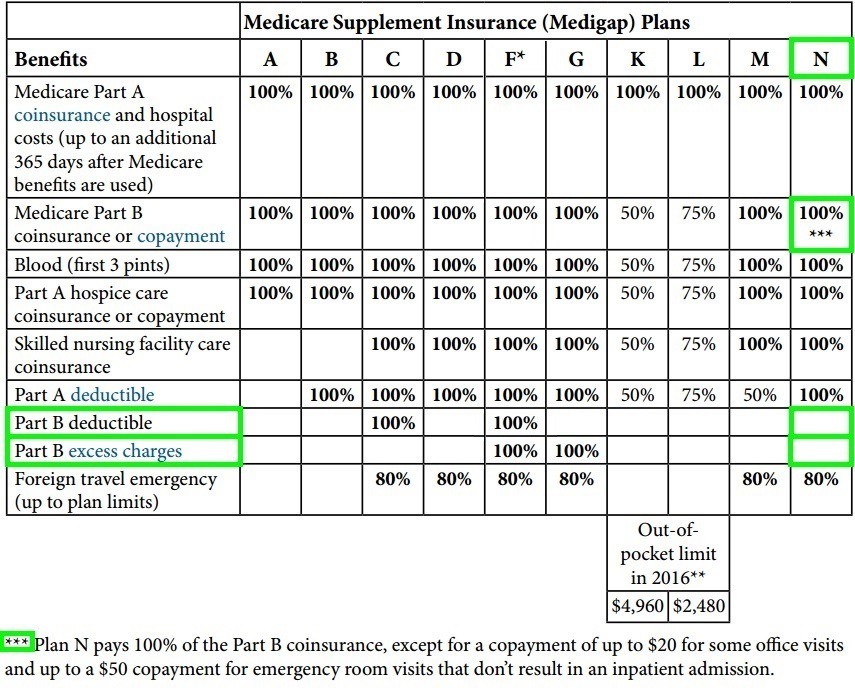

You can see Plan N highlighted in the chart below:

There are a few differences with Plan N compared to Plan F that you need to be aware of:

- You have a $183 annual Medicare Part B deductible that you’re responsible for (in 2017). So in order for Medicare to pay their part of any Part B related costs (other than certain preventative services, which Medicare covers at 100%), you’re responsible for meeting this $183 deductible first.

- Plan N has maximum copays of $20 for some office visits and $50 for emergency room visits. These copays can often be less than $20, especially for visits to your primary care physician. Also, unless there’s a doctor’s visit that accompanies seeing a chiropractor or physical therapist, you should not usually have to pay a copay for these visits.

- Plan N does not cover Medicare Part B excess charges. This means that if a healthcare provider does not accept Medicare’s billing amount (assignment), they can charge an additional amount for their Part B related services. Although these situations come up few and far between, be aware that there is a possibility of these additional expenses under Plan N.

Also, just like with most other Medigap plans, Original Medicare does not cover you outside of the country (except in rare cases), but your Plan N covers 80% of your expenses. However, before Plan N pays, you do need to meet a $250 deductible first. Also, any Medigap plan you have will have a lifetime benefit maximum of $50,000 for these foreign travel expenses.

Also, keep in mind, Medigap plans sold after 2005, like Plan N, don’t cover prescription drugs anymore.

So why is Plan N so much better of a deal than Plan F?

Plan N Doesn’t Have Plan F’s Problems

You can read here about the 3 reasons Plan F is too expensive. Plan N doesn’t have any of these 3 issues. This results in a lower amount of claims per Plan N member, which keeps the premiums low as well.

Also, let’s take a look at several examples at how Plan N rates stack up to Plan F.

65 Year-old Male in 48035:

Lowest Plan F: $145.52

Lowest Plan N: $103.52

SAVINGS: $42.00/month

69 Year-old Female in 46385:

Lowest Plan F: $123.44

Lowest Plan N: $82.94

SAVINGS: $40.50/month

73 Year-old Male in 24025:

Lowest Plan F: $143.86

Lowest Plan N: $97.33

SAVINGS: $46.53/month

You can see how much less the monthly premiums are with Plan N compared to Plan F. For example, a 65 year-old Male in 48035 can save $42/mo., or $504 per year in premiums with Plan N instead of F. Over time, you can see how you can save several hundred dollars each year in premiums and keep your potential out-of-pocket expenses fairly low.

Want to discuss your situation with a Medicare expert? Click the button to book a FREE personal 1-on-1 consultation.

Conclusion

Plan N is Medicare’s newest Medigap Plan. And even though your potential out-of-pocket expenses are not fixed, you’ll likely save money each year compared to being insured with Plan F. Have a Plan F now? Give me a call or send me an email to see how much you can save with Plan N.

Just getting on Medicare Part B for the first time? Maybe Plan N is the best fit for you.