What is it?

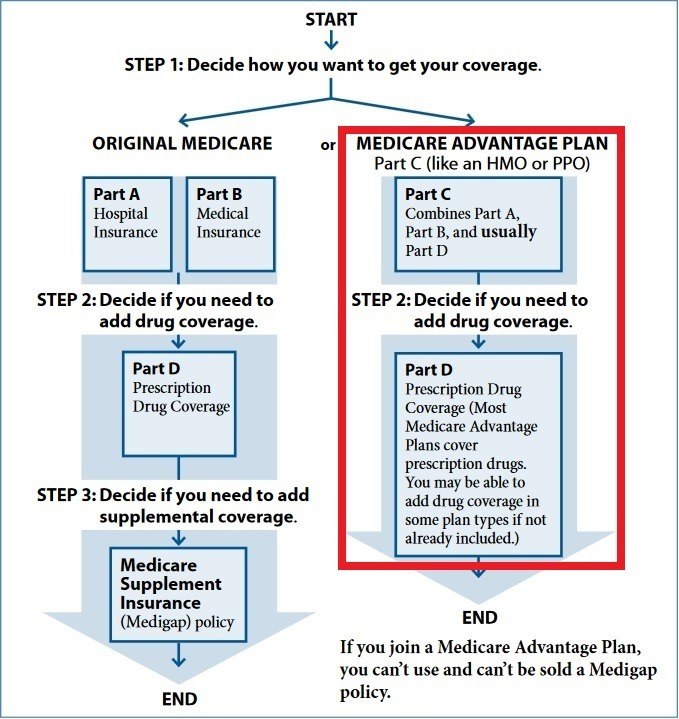

Medicare Advantage (MA) plans are also known as Part C of Medicare. What makes them different from Part A and B, though, is that they are offered through private insurance companies and not the federal government. In order to have an MA plan you have to be enrolled in both Parts A and B of Medicare. If you enroll in an MA plan, you are basically disenrolling from Original Medicare while you’re enrolled in the plan. Instead, your Part A and B coverage will be provided by the plan. During certain periods of the year you can disenroll from the MA plan and be back under Original Medicare. MA plans can be seen on the right in the block diagram below:

Because the MA plan now provides your managed health care, you have to follow their rules when it comes to receiving your health care. All MA plans will have a network of doctors, hospitals, and other health care providers that participate in the plan. If you go outside of this network, you will either not be covered or will often have to pay higher out-of-network rates. Just keep in mind if you are ever out of network, you’ll be covered as if you were in-network if you have a medical emergency and either need to go to the ER or to urgent care.

What Does it Cover?

Anytime you enroll in an MA plan, it has to cover everything that you would receive under Parts A and B of Medicare. However a small exception to this rule is that Original Medicare still covers hospice care for MA enrollees. However, this doesn’t mean your cost sharing would be the same for all your services as it would be under Original Medicare; the costs are discussed below.

MA plans will often have prescription coverage (Part D) as part of the plan. MA plans that have prescription coverage are often called MAPDs. So no matter if you go to your primary doctor, get admitted to the hospital, or go pick up a prescription at the pharmacy, with these plans you would show the same ID card at each location. It’s also important to note that you do not have to show your red, white, and blue Medicare card along with your MA or MAPD card when checking in for your health care services. Do not discard your Original Medicare card, but simply put it away for safe keeping in case you ever decide to switch from your MA plan back to Original Medicare.

MA plans will often throw in added benefits that are not covered under Original Medicare. These types of benefits include routine vision, dental, and hearing coverage. The plan may still often have a co-pay for these types of services, but generally at a reduced rate to what you would normally have to pay for them without this insurance. However, they will still require you to use their network providers in order to receive their lower cost benefits.

There are several types of MA plans and they all will work a little differently:

Health Maintenance Organization (HMO)

With pure HMOs, you have to go to a network doctor, hospital, facility, etc. in order to be covered. The only way you’ll be covered if you receive health care services out-of-network is if you need emergency care, need to go to urgent care, or receive dialysis. HMOs usually require you to choose a primary care physician (PCP) and you’ll need to get a referral to a specialist. However, some HMOs do make exceptions for some of these cases allowing you to receive some care from some providers without referrals, or allowing you to go outside of the network to receive certain services, but usually at a higher cost. An HMO that allows you to go out of network on a limited basis is called an HMO-POS, where POS stands for “point of service”.

Preferred Provider Organization (PPO)

PPOs typically allow you to receive your health care out-of-network if you prefer, but you’ll still pay higher out-of-network rates to do so. Unlike HMOs, however, PPOs don’t require you to get referrals to see specialists. All in all, PPOs typically have more freedom and flexibility compared to HMOs, but usually have a higher monthly premium compared to HMOs when comparing PPO and HMO plans with similar deductibles and co-pays side by side.

PFFS, MSA, SNP, PACE, etc.

There are several other types of MAs, MAPDs, or Medicare health plans, but in my experience I don’t come across them very often. Some of them require you to meet certain conditions to qualify to get the plan. If you would like to learn about them more in depth, check out: https://www.medicare.gov/sign-up-change-plans/medicare-health-plans/medi...

How Much Does it Cost?

Monthly premium

First of all, keep in mind that in order to have an MA plan you have to have both Parts A and B of Medicare. So you’ll have to pay the premiums for those. Next, some MA plans do not require an additional monthly premium, although many of them do. “How is it that an insurance company can give me a health care plan and not charge me a monthly premium”, you may ask? Well every time a Medicare beneficiary enrolls in an MA plan, Medicare provides funding to that plan to provide for that person’s health care. So the insurance company is effectively receiving a portion of your Medicare dollars, and then is responsible for providing your managed care plan.

MAPDs divide their cost share amounts into either the health care side of things (doctor, provider, hospital, etc.), or prescription side (Part D). Also, with all the cost shares listed below, they will often be higher if you choose to use out-of-network providers compared to those in network. This could apply for deductibles, coinsurance and copay amounts, and maximum-out-of-pocket amounts.

Deductible

Some MA and MAPD plans have deductibles and some don’t. There can be deductibles on the health care component and/or the prescription component. Again, a deductible is essentially your part of the cost sharing that you pay in full before the insurance kicks in and starts to pay its part. Each of these two types of deductibles would have to be met separately, so if you had a hospital stay, for example, and had to meet a deductible for this, you would have to meet a separate deductible when you go fill your prescriptions at the pharmacy.

Coinsurance and Copays

These terms are fairly similar and both mean that you and the insurance company pay together and that the coinsurance or copay is your part. Coinsurance is typically given as a percentage that you’re responsible for, where copays are generally a flat dollar amount you owe. Also, copays are often charged up front before you receive the good or service, and can apply both to health care (e.g. copay for doctor’s office visit) or prescriptions (e.g. copay for a 30-day prescription supply).

Maximum-Out-Of-Pocket (MOOP)

All MA and MAPDs have this MOOP. This is your max out of pocket amount that you’re liable for in any given calendar year. Once your deductible, coinsurance, and copays (but not premiums) total up to this maximum amount, you’ll pay nothing for covered services for the rest of the year. This MOOP does not apply towards Part D cost shares in your plan, as there is no maximum limit of how much you could spend for your prescription costs. I’ll cover this in more detail in the Part D section.

How Do I Pay For it?

If your MA or MAPD plan has a monthly premium, you typically have several payment options: it can be deducted from your Social Security income, deducted from your bank account, you can pay using a credit card, or can pay a direct bill every month. For the deductible and co-insurance amounts, you’ll generally be billed directly by the provider or facility where you receive healthcare services. Regarding co-pays, you’ll often have to pay them up front at the time of service.

How do I Sign Up?

You can sign up several ways including calling Medicare directly, calling the insurance company directly, enrolling through the Medicare.gov website’s Plan Finder, enrolling with the assistance of an independent insurance agent, etc. This is not a comprehensive list, but the important thing to remember is that the plan, its premium, and all of its cost shares and coverage is exactly the same no matter how you sign up. One of the main reasons to use an independent insurance agent that can represent many companies is that that agent can show you a wide variety of different MA plans available along with Medigap plans available in your area and answer your questions so you can make an educated decision on which one is best for you. You can check out my page about choosing the right plan on how to make an informed decision.

When Will it Start?

Your plan can start as soon as both Part A and Part B are effective, and no sooner. The effective date of your plan will also depend on the day you apply for it and the specific enrollment period you’re in. Click the link for more detail.

Do I Have to Sign Up?

Unlike Parts A and B that have potential late enrollment penalties, Part C has no such penalties. Also, you cannot sign up for both a Medigap plan and a MA plan, so if you decide a Medigap plan is best for you, you would not be enrolling in a Part C. It’s best to discuss your options with an independent insurance agent, like myself, who represents both MA and Medigap plans as well as several companies that offer each type. Contact me to request a time to talk and review your options.