You probably don’t understand insurance, right?

I don’t blame you, insurance can be pretty boring and confusing stuff. Especially health insurance.

Who’s going to sit there and go over your monthly health insurance statement and try to figure it out? There are so many numbers to try and understand and keep track of. And what’s the difference between a copay and co-insurance? Why is the deductible different than the max-out-of-pocket?

Well it’s hard to be comfortable with Medicare or your secondary insurance coverage if you don’t understand it at all.

Let’s take a look at some basic insurance terms and how they apply to Medicare and Medicare plans, so you can get a better grasp on how your plan works...

More...

Get a quote on Medigap plans in your area

Premium

This is the amount that you pay each month just to have the insurance. Even if you never use the insurance at all, you still pay the premium so you have that coverage if you ever need it.

You pay a monthly premium for Medicare. Some folks think that Medicare is free, but it’s not. Yes, you have had to pay a small amount out of each paycheck towards Medicare throughout your working life, but there is still a premium left to pay once you actually get on and use Medicare.

In this article I'm going to color-code your out-of-pocket expenses for both Medicare and Medicare plans. The colors for the different Parts and Plans will be:

- Original Medicare Parts A & B (blue)

- Medicare Advantage Plans (purple)

- Medigap Plans (green)

- Prescription Drug Plans (orange)

Original Medicare is Part A and Part B. The greatest majority of folks on Medicare do not pay a premium for Part A, and pay somewhere between $110 - $134 per month for Part B.

If you get a Medigap plan or prescription drug plan (PDP), you’ll owe a premium for it too. The amount depends on lots of things including your age, your zip code, and plan that you get.

With Medicare Advantage plans, there are some that you actually don’t have to pay an additional premium for. However, you still need to pay any Part A and Part B premiums you owe to be covered. Most of the Medicare Advantage plans do have a premium though.

Deductible

A deductible is technically something that you pay in full before the insurance pays anything out of their pocket. But, that doesn’t mean that you don’t get some benefits even before your full deductible is met.

With Original Medicare and Medicare Advantage Plans you get full coverage for various preventative services. Medicare, or your Medicare plan, has a certain list of things they cover at 100% even before you meet any deductible. So these preventative services are always free for you.

Taking advantage of your FREE Medicare preventative services is one of my 31 tips to save money on Medicare. Interested in learning about 30 others? Get your copy of my FREE e-book "31 Ways To Save Money on Medicare"

Medicare has a deductible for both Part A and Part B. The only time you’re responsible for the Part A deductible is if you ever get admitted to the hospital. This deductible is $1,316 (in 2017). This means that you’re responsible for the first $1,316, and then Medicare would pay the rest for “hospital-related” expenses during your stay for the first 60 days.

The Medicare Part B deductible is $183 (in 2017), which you’re responsible for paying in full for anything “medical-related” before Medicare starts to pay anything.

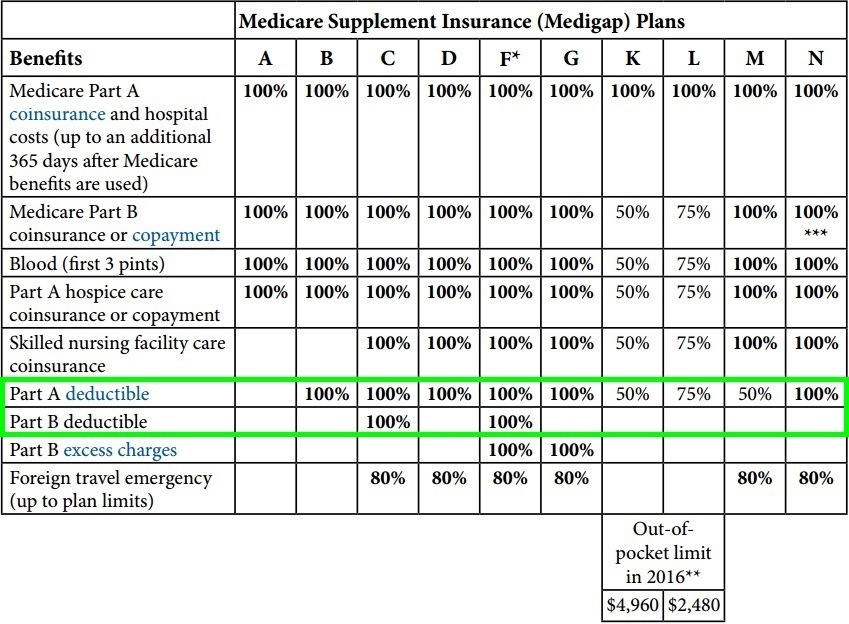

Medigap plans don’t really have deductibles. What they do is either cover, or don't cover, Medicare Part A or Part B deductibles. So if the Medigap Plan you have has a deductible, then it simply is not paying that specific Medicare deductible for you; instead you’re responsible to pay it. Take a look at the Medigap chart below to see which plans cover which Medicare deductibles.

PDPs may or may not have a deductible. Usually the plans that have lower premiums have higher deductibles, and higher premium plans tend to have no deductibles. This year (2017) the largest a PDP deductible can be is $400.

Medicare Advantage Plans also may or may not have a deductible, where the higher premium plans tend to have no deductibles. Since these plans usually combine medical and prescription coverage, they could have a separate deductible for each.

Copay and Coinsurance

These two terms are very similar. Regarding anything Medicare-related, these amounts now kick in once the deductible is met and the insurance company starts to pay its share. The main differences between the two are:

- Copays are usually flat dollar amounts ($50 for an office visit, for example), whereas a co-insurance is usually a percentage (your coinsurance can be 20%, for example) and can tend to be a lot higher actual dollar amount

- Copays are often due at the time of the visit, whereas you’ll often get a bill later for your part of the coinsurance

With Medicare, there is a Part B coinsurance. Once you meet the Part B deductible, Medicare starts to pay its share, which is 80%. So your responsibility is the other 20%, which is the coinsurance. The biggest gap in coverage under Original Medicare is this Part B coinsurance, because it has no dollar limit on the amount you’re responsible for.

Also, there are copays with Medicare Part A. If you have an inpatient hospital stay where you are still admitted after 60 days from the first day you were admitted, now you'll have daily copays to pay for. For a skilled nursing facility, there are copays for days 21-100 you are a resident; Medicare picks up the tab for the first 20 days.

Just like with the deductibles, Medigap insurance pays the Medicare copays and coinsurance amounts for you, depending on the plan. Again, refer to the Medigap chart above to see at what percentage the different letter plans pay these different amounts.

PDPs have copays and coinsurance amounts for the various covered medications depending on what “tier” the drug is in. The higher the tier number, typically the higher the amount you have to pay. Your out-of-pocket amounts are also based on what “phase” of coverage you’re in with your PDP for that calendar year. It can get pretty complicated, but just realize that you’ll almost always have to pay either a copay or coinsurance amount when you need to get a prescription filled.

Medicare Advantage Plans almost always have a copay or coinsurance amount every time you use them. If Original Medicare would cover something at 100%, then the Advantage Plan usually does not charge anything either. Sometimes these plans even include routine visits from certain doctors at no charge. But you almost always have something to pay out of pocket every time you use this coverage, whether you have a visit with a specialist, spend a day or two in the hospital, or get your generic prescriptions filled at your pharmacy.

Maximum Out-Of-Pocket

The maximum out-of pocket (MOOP) amount is how much you're responsible for in any given calendar year.

With Original Medicare, there is no MOOP. There's no limit on how much you're responsible for. As was mentioned in the coinsurance section above, with Original Medicare alone, you're responsible for 20% of all Part B charges.

Since Medigap policies pay the Medicare cost-sharing amounts for you, they limit your MOOP according to what plan you have. So for example, Plan G covers everything but the Part B deductible. This means the MOOP with Plan G is the Part B deductible of $183 (in 2017).

Every Medicare Advantage Plan is required to have a MOOP. This MOOP is for hospital and medical services only, not prescription coverage. This amount is usually dependent on whether you stay in-network for all your healthcare services, or if you go out-of-network at all. As an example, your in-network MOOP for the year might be $6,400, whereas your MOOP out-of-network might be $10,000.

PDPs do not have a MOOP. However, once you reach Phase 4 of your PDP for that calendar year, the most you'll be spending for any expensive medications will be 5% of their retail cost the rest of the year.

Conclusion

I hope these explanations and illustrations have helped you understand your cost-sharing responsibilities under Medicare and Medicare plans at least a little better. As always, let me know if you have any questions about these concepts.